Introduction

Space logistics and on-orbit servicing (OOS) cover the full ecosystem of in-space transportation, refueling, repair, inspection, debris removal, and manufacturing that keeps satellites functional and extends their working lives. The problem driving demand is straightforward: 10 to 20 GEO satellites are retired every year not because they've failed, but because they've run out of fuel.

That matters financially. Over 95% of the $100 billion generated annually in commercial satellite revenues comes from GEO assets, making life extension services an increasingly hard economic case to ignore.

2026 is where that economic case meets operational reality. After years of demonstrations, the industry is crossing from proof-of-concept into actual service delivery: four U.S. government-backed refueling missions are launching, private capital is flowing into debris removal, and in-space manufacturing is generating real revenue. China's successful GEO refueling demonstration in 2025 sharpened that urgency — it accelerated American investment and pushed Space Force doctrine toward dynamic space operations in ways that no domestic milestone had managed to do.

Key Takeaways

- On-orbit refueling transitions from experimental to operational in 2026, with four U.S. government missions demonstrating GEO servicing capabilities

- Active debris removal is now a strategic necessity — SDA's $52.5M contract to Starfish Space marks real government buy-in

- In-space manufacturing moved from concept to contract in 2025, with Varda's $187M Series C backing scaled orbital drug production

- Government agencies anchor the market, but industry needs clearer long-term funding and program-of-record commitments

- Shared "gas station" infrastructure models are reshaping the cost economics of sustainable on-orbit servicing

On-Orbit Refueling Transitions from Demonstration to Operational Service

On-orbit refueling means transferring propellant—typically hydrazine—to a satellite in orbit that is running low on fuel, extending its useful life by years without requiring a costly replacement launch. For GEO satellites that can cost hundreds of millions of dollars and serve critical communications and defense missions, life extension represents enormous value preservation.

The competitive landscape shifted in 2025 when China's Shijian-21 and Shijian-25 spacecraft performed the first-ever on-orbit refueling in GEO. The two spacecraft docked in mid-2025, performed fuel-intensive orbital plane changes, then separated in November. The demonstration confirmed the technology is operationally viable and raised strategic urgency for the U.S. to accelerate its own capabilities.

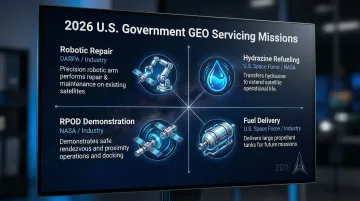

The U.S. response includes four government missions planned or launching in 2026:

Northrop Grumman SpaceLogistics' Mission Robotic Vehicle (MRV/RSGS): Equipped with robotic arms developed by the Naval Research Laboratory, the MRV performs inspection, repair, and installation of Mission Extension Pods (MEPs) on GEO satellites. MEPs are 350-kilogram propulsion "jet packs" that attach to a satellite's engine nozzle and provide roughly six years of additional life via electric propulsion.

Astroscale U.S. Refueler (APS-R): Launching in summer 2026, this mission will perform the first-ever hydrazine refueling operation in GEO, docking with a Tetra-5 satellite to transfer fuel.

Tetra-5: A constellation of Space Force/Air Force Research Lab prototype spacecraft demonstrating autonomous rendezvous, proximity operations and docking (RPOD), inspection, and receiving fuel.

Kamino (DIU): A Defense Innovation Unit satellite system carrying hydrazine fuel intended for transfer and delivery to refuel other satellites in GEO.

Taken together, these missions point toward a shared servicing model rather than custom solutions for each operator. Northrop's SpaceLogistics captures this logic well: the MRV can attach an MEP to one GEO satellite bus, restore its maneuverability, then move on to the next client. Repeating that process across multiple satellites spreads fixed infrastructure costs and makes each individual servicing operation more economical.

Why GEO Is the Priority for Refueling Economics

GEO satellites are larger, more expensive, and cover wider service areas than LEO counterparts, making repair and life extension cost-effective at scale.

A single GEO communications satellite can cost $200–400 million to build and launch, serving continental coverage areas for 10–15 years. When that asset runs out of fuel but remains otherwise functional, a $20–50 million servicing mission is a straightforward value calculation.

By contrast, smaller LEO satellites—often costing $500,000 to $5 million each—make the cost-to-service ratio far less attractive. COSMIC's Greg Richardson captured this with the "gas station" analogy: "When you go and fill up, you don't have to buy an entire gas station to fill up your car... You buy the gas that you need, and some fraction of that cost pays the overhead and fixed costs. That's what you want to do in orbit." A shared servicing infrastructure in GEO allows many client satellites to share fixed costs rather than each operator building custom servicing infrastructure.

Deorbit & Active Debris Removal Emerges as a Strategic Necessity

With satellite constellations growing rapidly, deactivated satellites in LEO can take decades to naturally re-enter the atmosphere, creating collision risk and orbital congestion. The ESA Space Environment Report 2025 notes that space surveillance networks regularly track about 44,870 space objects, with approximately 11,000 being active payloads. The actual number of debris objects larger than 1 cm exceeds 1.2 million. At 550 km altitude, the density of debris objects posing threats is now the same order of magnitude as active satellites.

For the military, the urgency is real. The Space Development Agency now requires end-of-life satellites to be disposed of within 1 year — or as little as 6 months — rather than leaving them to drift for decades. This protects orbital slots and reduces collision threats to active military assets.

That mandate translated into real spending. In January 2026, SDA awarded Starfish Space a $52.5 million contract for Deorbit-as-a-Service, covering end-of-life disposal for Proliferated Warfighter Space Architecture (PWSA) satellites.

Economics remain the hard constraint. As SDA's Ryan Wolff noted, a $100 million servicing mission for a $14 million satellite doesn't make economic sense. Closing that gap requires standardized, lower-cost removal vehicles — the central engineering challenge the industry hasn't fully solved yet.

Private capital is starting to weigh in. Starfish Space raised over $100 million in Series B funding in April 2026, led by Point72 Ventures, to execute contracted Otter deorbit missions. The raise reflects investor confidence that debris removal can become a repeatable commercial business — not just a government-funded proof of concept.

In-Space Manufacturing and Cislunar Supply Chains Take Shape

In-space manufacturing is moving from concept to commercial reality. Varda Space Industries successfully recovered its third in-space capsule (W-3) at South Australia's Koonibba Test Range on May 13, 2025, carrying an advanced inertial measurement unit developed with the U.S. Air Force.

That momentum carried into July 2025, when Varda secured $187 million in Series C funding to scale orbital pharmaceutical manufacturing—proof that microgravity production has crossed from experiment to investable business.

NASA's 2025 awards reflect structured supply chain thinking for beyond-LEO missions:

- Blue Origin received a $190 million CLPS task order in September 2025 to deliver the VIPER rover to the Moon's South Pole in late 2027 using the Blue Moon Mark 1 lander

- Sierra Space received a $3.6 million NextSTEP-2 contract in May 2025 to study expandable space station technology for lunar surface logistics and mobility

Taken together, these awards shift space logistics from a maintenance function into an economic production layer. Supporting that layer means infrastructure designed for far more than satellites — think crewed habitats, manufacturing facilities, and in-situ resource use, each requiring storage, waste management, and supply chain continuity beyond Earth orbit.

Government as Anchor Customer — Demand Signals Drive Commercialization

Government agencies—Space Force's Space Systems Command, DARPA, DIU, NASA, and ESA—are acting as the first paying customers for on-orbit services, providing the revenue certainty that allows commercial companies to invest in scalable infrastructure. The dynamic echoes how early government aviation contracts gave commercial airlines the financial footing to grow.

Industry leaders, however, are flagging a critical gap. At SATShow 2026, executives from Astroscale, SpaceLogistics, and Trident Solutions agreed that moving from "one-offs" to true operational infrastructure requires a program-of-record with committed, sustained funding—not just pathfinder contracts.

"We have the technology to be able to do it... We just need that program of record to say 'We actually want to fund that going forward.'" — Robert Hauge, President, Northrop Grumman SpaceLogistics

John Moberly of Trident Solutions pushed for a concrete policy fix: shifting RDT&E funding to O&M (Operations and Maintenance) to acquire and deploy servicing capabilities without waiting for new program approvals. This funding flexibility is a central policy focus for 2026–2027.

Standardization and Interoperability — Building the "Universal Adapter" for Space

Just as a meeting room requires HDMI, USB-C, or a dongle depending on the device, satellite servicing vehicles need to know what interface a client satellite uses before a mission. Lack of standardization adds cost and complexity, forcing custom engineering for each client.

Progress is emerging. Three milestones mark the current direction:

- Northrop Grumman's Passive Refueling Module (PRM) — Selected by Space Systems Command in January 2024 as the first preferred refueling interface standard for SSC satellites

- Orbit Fab's RAFTI — Designated by SSC in August 2024 as an accepted refueling interface for military satellites

- ANSI/AIAA S-157-2025 — Published by AIAA in March 2025, defining best practices for in-space storable fluid transfer systems

The industry isn't converging on a single mandated port design, but these efforts are establishing practical common standards that servicing vehicles can be built around. Servicing vehicles only become cost-effective at scale when they don't need custom engineering for every mission — and that's exactly what these standards make possible.

What's Driving These Space Logistics Trends

Space logistics is not advancing due to any single driver but due to simultaneous pressure from geopolitical competition, military operational needs, commercial satellite economics, and maturing enabling technologies. The global on-orbit satellite servicing market is projected to grow from $4.67 billion in 2025 to $12.60 billion by 2035, a CAGR of 10.43%.

Autonomous rendezvous and proximity operations (RPOD) have matured steadily, crossing several concrete milestones:

- DARPA's Orbital Express demonstrated on-orbit refueling in LEO in 2007

- Northrop Grumman's MEV-1 and MEV-2 successfully docked with operational commercial satellites in GEO in 2020 and 2021

- The Naval Research Laboratory's robotic manipulation arm, featuring dual arms with lights, cameras, and tool changers, completed thermal vacuum testing in September 2025 and is integrated onto Northrop's MRV for 2026 launch

AI-driven anomaly detection and advances in miniaturized propulsion have made on-orbit servicing mechanically feasible.

China's 2025 GEO refueling milestone created tangible urgency for the U.S. military. Dynamic space operations—satellites maneuvering to approach or avoid adversary assets—consume fuel rapidly, making on-orbit logistics a warfighting enabler, not just a cost-saving tool.

Frequent, lower-cost launch access is lowering the barrier to placing servicing vehicles in orbit. Innovations in propulsion—including non-rocket approaches like Green Launch's hydrogen/oxygen light-gas system—are pushing down the cost of getting payloads to orbit efficiently and sustainably. Green Launch's technology offers a rapid launch cadence (every 60-90 minutes) at projected costs of $100/lb to LEO. That enables just-in-time delivery of small satellites, propellant modules, and supplies to orbital depots—particularly valuable for servicing missions requiring emergency deployment.

How These Trends Are Reshaping the Space Industry & Future Signals Through 2027

Industry and Operational Impact

Satellite operators are beginning to design satellites with serviceability in mind rather than treating them as single-use assets. The acceptance of standard interfaces like Northrop's PRM and Orbit Fab's RAFTI is driving this shift—future satellites can be designed to receive fuel while in space, enabling sustained maneuverability. This changes procurement, insurance, and operational planning across both commercial and government sectors.

Business models are shifting toward "service as infrastructure." The gas station model and MEP-as-a-service offerings mean capital expenditure on satellite assets can be stretched over longer timelines, improving ROI and opening new insurance and financing structures. Operators can plan for 20–25 year asset lifespans instead of 10–15 years — a shift that rewrites fleet management economics from the ground up.

Where these trends lead depends on what the next 18 months actually prove in orbit.

Future Signals to Watch (2026–2027)

Near-term technical milestones: Results from the four 2026 GEO servicing missions will be the most important data points for the industry. Success validates the business case; anomalies or delays will reveal which engineering gaps remain, particularly around autonomous docking and propellant transfer. As Lt. Gen. Philip Garrant noted, "One of the biggest things that we want to get out of it is to help us flesh out the requirements and [concept of operations] and understand the real feasibility... Is this a good business case?"

Policy and funding signals: Watch for whether any of the 2026 pathfinder missions graduate to a formal program of record in the FY2027–2028 defense budget cycle. This would be the clearest signal that the U.S. government is committed to operationalizing space logistics rather than perpetually demonstrating it.

Longer-term watch: Three developments will indicate the space logistics economy has moved beyond government dependency:

- Cislunar logistics standards adopted across operators

- In-space manufacturing scale-up, including Varda's Series C deployment

- The first commercial (non-government) refueling transaction completed on a paying basis

Conclusion

Space logistics and on-orbit servicing are no longer emerging concepts. In 2026, refueling missions fly, deorbit contracts get awarded, and in-space manufacturing generates real revenue—all backed by government anchor customers and growing commercial investment.

For aerospace and defense organizations, satellite manufacturers, and space access providers, the window to enter this logistics ecosystem is open now. The organizations that move first won't just participate in the space economy; they'll set the terms for how it operates.

Frequently Asked Questions

What is on-orbit servicing and why is it important in 2026?

On-orbit servicing includes in-space capabilities like refueling, repair, inspection, and deorbit that extend satellite life and reduce the need for costly replacement launches. 2026 is significant because multiple operational missions are launching for the first time, transitioning the industry from proof-of-concept to real service delivery.

What types of satellites benefit most from on-orbit servicing?

Large, expensive GEO satellites used for communications, broadcasting, and military operations benefit most due to favorable cost-to-service economics: servicing missions costing $20–50M can extend the life of $200–400M assets. LEO servicing remains more limited to debris removal given lower per-satellite costs.

How does orbital refueling actually work?

A servicing vehicle like Astroscale's refueler or Northrop's MRV autonomously rendezvouses with the target satellite, docks, and transfers hydrazine or other propellant. Some missions instead install a Mission Extension Pod with electric thrusters, adding roughly six years of operational life.

What are the biggest obstacles to scaling a space logistics industry?

Three obstacles dominate: lack of satellite interface standardization requiring custom engineering per mission, no sustained government program of record beyond pathfinder contracts, and the cost-matching challenge. That last point is straightforward, ensuring servicing costs don't exceed what the target satellite is actually worth.

How is China's progress in on-orbit servicing affecting U.S. strategy?

China's 2025 GEO refueling mission elevated space logistics to a national security priority for the U.S. It has accelerated DoD investment in four 2026 servicing missions and shaped Space Force doctrine around dynamic space operations, where satellites must maneuver to approach or evade adversary assets.

What is active debris removal and how does it differ from satellite servicing?

Active debris removal focuses on capturing and deorbiting non-functional satellites or spent rocket bodies to reduce collision risk and orbital congestion. Satellite servicing extends the life of functioning assets through refueling, repair, or inspection. Both are part of the space logistics ecosystem but serve different operational and regulatory purposes.