Introduction

CubeSats—compact, standardized small satellites—have evolved dramatically from their origins as academic teaching tools into critical commercial and defense assets. What began as university-led experiments now drives commercial satellite constellations, defense reconnaissance systems, and global IoT connectivity networks — and the launch market hasn't fully caught up.

The central tension driving this market is straightforward yet consequential: demand for CubeSat launches is accelerating due to proliferating small satellite constellations, yet access to dedicated, affordable, and frequent launch services remains a bottleneck for many operators. Traditional rideshare missions offer low costs but constrain orbit selection and timeline flexibility. Dedicated small launch vehicles provide orbital precision but command premium pricing and face reliability challenges.

What follows covers market sizing, demand drivers across commercial and government sectors, launch vehicle trade-offs, regional activity, and emerging propulsion approaches — including hydrogen light-gas platforms — that could reshape small satellite access to orbit through 2026.

TLDR

- The CubeSat launch segment is expanding faster than the broader satellite launch market, driven by mega-constellations and government proliferated architectures

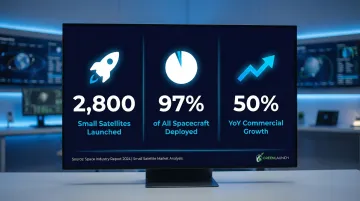

- Nearly 2,800 small satellites launched in 2024 alone, representing 97% of all spacecraft deployed and highlighting explosive demand

- Cost drives most launch decisions: rideshare pricing runs ~$7,000/kg, while dedicated launchers charge $19,000–$40,000/kg for orbital flexibility

- Hydrogen light-gas propulsion is gaining traction as a lower-cost, sustainable alternative for high-frequency CubeSat deployment

CubeSat Launch Vehicle Market Size and Growth Outlook for 2026

The broader satellite launch vehicle market is projected to reach $22.74 billion in 2026, expanding from $20.21 billion in 2025 at a 12.6% CAGR. Within this ecosystem, the small satellite segment is growing even more aggressively. The small satellite market is projected to surge from $9.35 billion in 2025 to $32.13 billion by 2030, representing a 28.0% CAGR—more than double the pace of the broader launch vehicle market.

Record Launch Activity Driven by Commercial Operators

Launch statistics from 2024 underscore this explosive growth trajectory. Nearly 2,800 small satellites (under 1,200 kg) were launched in 2024, accounting for 97% of all spacecraft deployed and 81% of total upmass. Commercial operators are driving this surge: commercial launches increased 50% year-over-year in 2023 compared to 2022, and by 2024, commercially operated rockets were responsible for 70% of global orbital launch attempts.

The shift from government-only programs to commercial operators has expanded the total addressable market for CubeSat launches. Commercial missions now represent the dominant share of all small satellite deployments, with operators building out constellations to support:

- Earth observation and remote sensing

- IoT connectivity and asset tracking

- Maritime and aviation monitoring

- Environmental and climate research

Pipeline Projections Through 2030

Looking ahead, Euroconsult projects that approximately 18,500 satellites weighing under 500 kg will reach orbit by 2031, adding up to roughly 365 tons per year of upmass. For providers focused on CubeSat-class payloads, that volume represents a structural shift in who needs launch access — and how often.

Key Drivers Fueling CubeSat Launch Demand

Proliferation of Small Satellite Constellations

Mega-constellation programs require frequent, scheduled launches for both initial deployment and ongoing replenishment. Operators must maintain satellite populations across specific orbital planes to keep services running—creating steady, predictable demand for affordable CubeSat-class launch services.

Key characteristics driving this demand:

- Spans Earth observation, IoT connectivity, maritime tracking, and environmental monitoring — demand is distributed across sectors, not tied to one

- Satellites in low Earth orbit face atmospheric drag and short operational lifespans, requiring continuous refresh missions

- Operators add satellites regularly to expand coverage and service capabilities

Government and Defense Investment

National space agencies and defense departments now rely on CubeSats for rapid-deployment reconnaissance, communications resilience, and technology demonstration missions. Government procurement reflects this strategic shift toward proliferated space architectures.

Recent government commitments illustrate the scale of this demand:

- SDA Tranche 3: In late 2025, the Space Development Agency awarded four contracts totaling ~$3.5 billion to build 72 Tracking Layer satellites

- Space Force/SpaceX: The U.S. Space Force awarded SpaceX $739 million in launch orders under the NSSL Phase 3 Lane 1 program to support SDA and NRO deployments

- NASA CSLI: The CubeSat Launch Initiative has launched over 150 CubeSats since inception, with solicitations open for the 2026–2029 pipeline

Cost economics reinforce this trend. Falling launch prices have made proliferated architectures financially practical for both government and commercial operators alike.

Falling Launch Costs and Increasing Launch Cadence

The entry of multiple dedicated small launch vehicle providers has driven competitive pricing pressure across the market. Cost reduction trends are evident when comparing rideshare versus dedicated launch economics:

Cost Benchmarks (2024-2025)

| Service Type | Provider Example | Cost per Kilogram | Notes |

|---|---|---|---|

| Rideshare | SpaceX Transporter | $7,000/kg | Base price $350,000 for 50 kg to SSO |

| Dedicated Small Launch | Rocket Lab Electron | $37,500–$40,000/kg | ~$7.5M-$8M for 200 kg payload |

| Dedicated Small Launch | Firefly Alpha | $18,400–$30,100/kg | $19M for 630 kg to SSO or 1,030 kg to LEO |

Reusability has reshaped launch economics. Falcon 9's partially reusable design dropped costs from ~$10,000/kg to ~$2,500/kg—a 75% reduction—making large-scale satellite constellations commercially practical.

Dedicated Launch vs. Rideshare: Choosing the Right Option for CubeSat Operators

The choice between dedicated launch and rideshare comes down to a single trade-off: orbital control versus cost. Here's how the two pathways compare:

Dedicated small launch vehicles fly a single customer's payload to a customer-specified orbit, offering orbital flexibility, faster scheduling control, and preferred insertion parameters—but typically at higher cost per mission.

Rideshare missions aggregate multiple payloads onto a single larger vehicle. SpaceX's Transporter program is the dominant example: lower per-kg cost and high reliability, but orbit choice and mission timeline follow the primary customer's needs.

The Rideshare Dominance: SpaceX Transporter

SpaceX's Transporter program commands the Western smallsat rideshare market. SpaceX has launched more than 1,000 smallsats across its rideshare program, with no comparable Western competitor at scale. The program maintains a regular cadence, though entry price has increased from the original $5,000/kg to $7,000/kg, reflecting SpaceX's market power and sustained demand.

Dedicated Small Launch Landscape

Despite rideshare dominance, dedicated small launchers maintain a critical niche for operators requiring specific orbital insertions:

- Rocket Lab Electron: The most prolific dedicated small launcher, Electron has flown 85 times since May 2017, with 81 successes and 4 failures. In 2024, Rocket Lab achieved a record 16 Electron launches.

- Firefly Alpha: A mixed but improving record — 7 total launches (3 successes, 2 failures, 2 partial failures) — with a successful return to flight in March 2026.

Bridging the Gap: Orbital Transfer Vehicles

For operators who want rideshare pricing without surrendering orbital flexibility, orbital transfer vehicles (OTVs) offer a third path. These space tugs allow CubeSat operators to purchase a rideshare slot and still reach a custom orbit through post-deployment maneuvering — directly softening the core trade-off between the two primary pathways.

Key players include:

- D-Orbit operates its ION Satellite Carrier for in-space transportation and hosted payload missions

- Exolaunch deploys satellites on SpaceX Transporter missions using its EXOpod deployers, with full integration services

- Momentus has been developing its Vigoride space tug for in-orbit delivery, with multiple missions flown since 2022

OTVs don't eliminate the dedicated launch market, but they do compress the cost gap — giving operators more leverage when the rideshare orbit is close enough to their target that a tug can close the difference.

Regional Market Breakdown: Where CubeSat Launch Demand Is Concentrated

North America: Commercial Ecosystem Anchor

North America remains the dominant region in the global small satellite market, driven by extensive funding, government support, and private companies like SpaceX and Rocket Lab. U.S. operators have been responsible for 75% of all smallsats launched since 2015.

The region's advantages include:

- Mature commercial launch ecosystem with multiple providers

- Strong commercial CubeSat developer community

- Regular rideshare cadence through SpaceX Transporter missions

- Significant government procurement (NASA CSLI, SDA contracts, DOD missions)

That North American dominance faces its most direct competition from the east. Asia-Pacific has emerged as the highest-volume launch region by raw orbital attempt count, with several distinct national programs accelerating activity:

Asia-Pacific: Rapid Growth and Government Programs

- China: Conducted 68 orbital launches in 2024, slightly up from 67 in 2023, with commercial operators like LandSpace and CAS Space expanding rideshare capacity

- Japan: Deployed 25 payloads in 2024 across JAXA missions and commercial H3 rocket operations

- India: Launched 10 payloads in 2024, with ISRO's SSLV (Small Satellite Launch Vehicle) targeting the sub-500 kg market directly

- South Korea: Achieved first successful orbital launch of the domestically developed KSLV-II (Nuri) rocket in 2023, with commercial follow-on missions planned through 2027

Where Asia-Pacific competes on volume, Europe's priority is independence. The continent is investing in indigenous small launch capabilities specifically to reduce reliance on U.S. and Russian providers:

Europe: Sovereign Access and Commercial Emergence

- PLD Space (Spain): Awarded a €40.5 million PERTE contract by the Spanish government to develop the Miura 5 orbital launcher, with a commercial contract with Sateliot for a dedicated Miura 5 launch scheduled for 2027

- Isar Aerospace (Germany): Completed a static-fire test of the first stage of its Spectrum rocket in February 2025, awaiting a launch license from the Norwegian Civil Aviation Authority for its maiden flight from Andøya Spaceport

For CubeSat operators, Europe's maturing launch options mean a concrete alternative when U.S. rideshare schedules slip or export licensing creates delays — a recurring operational pain point for non-U.S. satellite developers.

Emerging Technologies Reshaping CubeSat Access to Space

Reusability Drives Down Launch Economics

Reusable launch vehicle technology has reshaped CubeSat launch economics. As reusability reduces per-launch fixed costs, providers can price rideshare and dedicated small-sat missions more competitively.

The cost reduction impact is most significant for medium and heavy-lift rideshare rather than dedicated small launch vehicles, where reusability technology is still maturing. Still, the 75% cost reduction achieved by Falcon 9's partial reusability has established market expectations for continued price pressure across all launch segments.

Non-Rocket and Alternative Propulsion Approaches

While vertical rockets dominate current launch operations, alternative approaches are entering the CubeSat launch conversation as potential disruptors:

Air-Launch Systems: Following Virgin Orbit's bankruptcy, the air-launch sector contracted, though Stratolaunch continues to expand the flight envelope of its Roc aircraft for hypersonic testing applications.

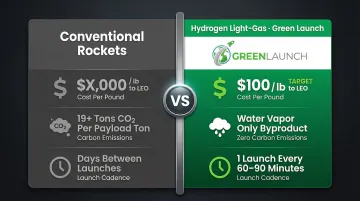

Hydrogen Light-Gas Gun Technology: Companies like Green Launch are developing proprietary light-gas propulsion systems using environmentally friendly hydrogen and oxygen propellants. This approach aims to deliver high-velocity, cost-effective payload delivery by using ground-based impulse launchers rather than traditional multi-stage chemical rockets.

The environmental profile of hydrogen light-gas systems sets them apart from conventional options. Traditional RP-1 and MethylOx rockets produce over 19 tons of CO2 per ton of payload delivered to orbit; hydrogen-oxygen combustion produces only water vapor.

Propellant capture technology achieves over 91% recovery efficiency, cutting both environmental impact and operating costs without the complexity of reusable rocket stages.

Green Launch's system has demonstrated projectile velocities of 2.97 km/sec (Mach 9) using one-stage light-gas combustion with precision gas injection. Key performance targets include:

- Launch cadence: one mission every 60–90 minutes ("next-day air delivery to space")

- Target pricing: $100 per pound to Low Earth Orbit

- Propellant byproduct: water vapor only, versus 19+ tons of CO2 per payload ton for conventional rockets

Advances in Satellite Manufacturing

Additive manufacturing (3D printing) is being applied to CubeSat buses to reduce weight and integration time. Multi-functional CubeSat buses with integrated internal lattices and wiring tabs offer new ways to optimize mass and schedule, indirectly amplifying demand for launch frequency and further motivating investment in faster, more flexible launch technologies.

Market Challenges and the Road Ahead

Persistent Barriers to Growth

Despite strong demand fundamentals, several barriers constrain CubeSat launch market expansion:

- Launch vehicle reliability: Even established providers experience anomalies, and newer entrants face steep learning curves. Schedule delays remain a consistent pain point for small satellite operators booking rideshare slots months in advance.

- Regulatory and spectrum licensing timelines: Approvals have not kept pace with commercial launch cadence. The FCC's 5-year deorbit rule for LEO satellites (down from 25 years, effective September 29, 2024) reflects orbital sustainability pressure, but coordination across international regulators adds friction.

- Orbital congestion and debris: As of 2024, approximately 35,000 objects are tracked by space surveillance networks — about 9,100 active payloads and 26,000 debris pieces larger than 10 cm. Two-thirds of active satellites cluster between 500 and 600 km altitude, creating collision risk hotspots that complicate new deployment approvals.

Market Consolidation and Startup Failures

The small launch market has faced severe financial headwinds — and the pattern is clear: providers who can't control burn rates without sacrificing reliability don't survive. Virgin Orbit filed for Chapter 11 bankruptcy in April 2023 after a failed launch and inability to secure long-term funding, eventually selling its assets. Astra Space struggled with cash flow, shelving its Rocket 3 vehicle and agreeing to be taken private by its founders in early 2024 to avoid bankruptcy.

These failures highlight a structural reality: capital efficiency alone isn't enough without a credible path to recurring revenue. Consolidation is likely to continue through 2026–2027, with providers that have dual-use applications or differentiated propulsion architectures showing the most resilience.

Forward-Looking Perspective

The next phase of this market will separate providers with genuine technical differentiation from those competing on price alone. Approaches like alternative propulsion architectures — including ground-based and non-chemical systems — are gaining attention precisely because they sidestep the cost floor that traditional rockets struggle to break through.

Success factors for the next phase include:

- Demonstrating consistent operational reliability across multiple launches

- Achieving competitive pricing through reusability or alternative propulsion architectures

- Meeting regulatory requirements while maintaining launch cadence

- Developing sustainable solutions for orbital debris mitigation

- Providing orbital flexibility through dedicated launches or OTV integration

Frequently Asked Questions

What is the current size of the CubeSat launch vehicle market in 2026?

The broader satellite launch vehicle market is projected to reach approximately $22.74 billion in 2026, with the CubeSat and small satellite segment representing a fast-growing share expanding at 28% CAGR through 2030. For segment-specific figures, consult market research from MarketsandMarkets or Bryce Tech.

What is the difference between a dedicated CubeSat launch and a rideshare mission?

Dedicated launches carry a single operator's payload to a chosen orbit on a small launch vehicle, while rideshare missions aggregate multiple payloads onto a larger rocket. Cost and orbit flexibility represent the primary trade-off: rideshare offers lower per-kg pricing ($7,000/kg) but limits orbital parameters, while dedicated launches provide precise insertion at premium cost ($19,000–$40,000/kg).

Which launch vehicles are most commonly used for CubeSat deployments?

Key dedicated small launch vehicles include Rocket Lab Electron and Firefly Alpha. Major rideshare platforms include SpaceX Transporter series, which has launched over 1,000 smallsats to date. ISS deployment via NanoRacks/Cygnus remains an option for operators with specific microgravity research requirements.

How is reusable rocket technology impacting CubeSat launch costs?

Reusability reduces fixed per-launch costs, which providers can pass on through lower rideshare pricing. Falcon 9's partial reusability drove a 75% cost reduction (from ~$10,000/kg to ~$2,500/kg), with the greatest impact on medium and heavy-lift rideshare — dedicated small launch vehicles are still working through the reusability curve.

Which regions are leading CubeSat launch activity in 2026?

North America and Asia-Pacific dominate, with U.S. operators responsible for 75% of all smallsats launched since 2015. China, India, and Japan lead Asia-Pacific activity. Europe contributes through ESA programs and emerging commercial providers like PLD Space (Spain) and Isar Aerospace (Germany).

What alternative launch technologies could disrupt the CubeSat launch market?

Light-gas gun systems, air-launch platforms, and electromagnetic accelerators are all under active development. Green Launch's hydrogen-oxygen impulse system is one example: targeting $100 per pound to orbit with potential launch cadences every 60–90 minutes, it aims to cut costs and reduce emissions compared to conventional rocket launches.