Introduction

As ESG and sustainability reporting obligations tighten globally — from IFRS S2 to the GHG Protocol — the environmental footprint of every operational activity is under scrutiny, including space launches. As of 2026, 36 jurisdictions have adopted or are finalizing IFRS S1/S2 standards, while the EU's Corporate Sustainability Reporting Directive (CSRD) requires companies to substantiate environmental claims using robust, science-based methods. In this tightening regulatory environment, aerospace-dependent companies must account for launch emissions with precision and transparency.

A zero-emission launch claim — based on propellants like hydrogen and oxygen whose combustion produces only water vapor — offers a legitimate pathway to reduce reported Scope 3 emissions. Credibility depends heavily on propellant verification, correct GHG scope classification, documentation standards, and the specific ESG framework being used.

Getting this wrong — even with the right propellants — can expose your organization to greenwashing risk under CSRD, SEC climate disclosure rules, or third-party audit scrutiny. This guide covers:

- What qualifies as a zero-emission launch under major ESG frameworks

- The step-by-step process for claiming it in a sustainability report

- Documentation and verification requirements to prepare in advance

- Common mistakes that can invalidate or undermine your claim

Key Takeaways

- Zero-emission launches use propellants whose combustion produces only water vapor, with no GHG Protocol-listed gases

- Claims must be classified under the correct GHG scope (typically Scope 3 Category 1 for third-party services)

- Auditor-ready documentation includes propellant specs, provider certifications, and methodology notes

- Major ESG frameworks (GRI, IFRS S2, GHG Protocol) each have specific disclosure requirements

- Document propellant and provider details before launch — retroactive claims are harder to verify and defend

How to Claim a Zero-Emission Launch in Your ESG and Sustainability Report

Step 1: Verify the Emission Profile of Your Launch Provider

Confirm the exact propellant type used by your launch provider and whether combustion byproducts include any greenhouse gases. Hydrogen-oxygen propulsion produces only water vapor, making it a legitimate basis for a zero-emission claim.

Green Launch's proprietary light-gas propulsion system uses hydrogen and oxygen gas as propellant, with water vapor as the only combustion byproduct — a profile that supports a direct zero-emission disclosure.

What to request:

- Propellant specification sheet with combustion chemistry data

- Technical documentation confirming exhaust composition

- Emission factor calculations (should be 0 kg CO2e for true hydrogen-oxygen systems)

- Information about supplemental fuels or pressurization gases

Note that liquid hydrogen and liquid oxygen (LH2/LOX) combustion produces 0 kg of CO2, 0 kg of black carbon, and 0 kg of alumina per launch, according to a comprehensive 2024 inventory of worldwide rocket launch emissions. However, check whether any staging operations or orbital circularization maneuvers require supplemental propulsion that could produce additional emissions.

Request third-party validation, environmental certifications, or published emission calculations from your provider. Green Launch, for instance, can supply propellant specifications and test series performance data from its Yuma Proving Ground firings to support your documentation package.

Step 2: Classify the Launch Under the Correct GHG Scope

Determine whether the launch falls under Scope 1, Scope 2, or Scope 3 emissions. This is one of the most common reporting errors and affects how auditors review your claim.

Classification rules:

- Scope 1: Only if you own or directly control the launch equipment

- Scope 3, Category 1: If you commission a third-party launch provider (most common scenario)

The GHG Protocol defines Scope 3, Category 1 as all upstream (cradle-to-gate) emissions of purchased goods and services. For a satellite operator contracting a launch, the emissions cannot be Scope 1 because you don't own or control the launch vehicle.

If using an external launch provider, document the supplier engagement and emission data sharing process. Scope 3 claims require evidence that the vendor-level emission factor is accurate and traceable.

The GHG Protocol's data quality hierarchy prioritizes supplier-specific methods over industry averages or spend-based estimates — so get that data directly from your provider, not from a proxy calculation.

Step 3: Gather and Organize Supporting Documentation

Compile required documentation before drafting your ESG report:

- Propellant composition records

- Launch logs and performance data

- Provider contracts or technical agreements

- Emission calculation methodology

- Supplier-specific cradle-to-gate emission factors

Confirm that documentation meets the documentation requirements of your chosen ESG framework. IFRS S2 requires measurement approaches and inputs that result in a faithful representation of Scope 3 GHG emissions, prioritizing data based on direct measurement and specific activities within your value chain.

Key transparency standard: The GHG Protocol requires that information be recorded, compiled, and analyzed in a way that enables internal reviewers and external verifiers to attest to its credibility. Build your documentation trail with that audit standard in mind before you draft a single line of your report.

Step 4: Draft the Disclosure Using Framework-Appropriate Language

Write the zero-emission launch claim within the applicable section of your report — typically the Scope 1/3 emissions inventory, climate-related disclosures, or environmental performance metrics. Use terminology aligned with your reporting framework:

Framework-specific requirements:

| Framework | Key Language Requirement |

|---|---|

| GRI 305 | "Gross direct (Scope 1) GHG emissions in metric tons of CO2 equivalent" |

| IFRS S2 | "Absolute gross greenhouse gas emissions generated during the reporting period, expressed as metric tonnes of CO2 equivalent" |

| GHG Protocol | "Total scope 1 and 2 emissions independent of any GHG trades" |

| TCFD | "Scope 1, Scope 2, and, if appropriate, Scope 3 greenhouse gas (GHG) emissions" |

Clearly distinguish between "zero greenhouse gas emissions" and related but distinct claims like "carbon neutral" or "net zero." A zero-emission launch based on hydrogen-oxygen propulsion is a direct emissions claim — not an offset-based claim. IFRS S2 strictly differentiates between gross and net targets, requiring separate disclosure of gross targets even when net targets exist.

Include a methodology note explaining how the emission factor of zero was derived. Cite the specific provider documentation and data sources that support it — this note is what gives the claim audit standing.

Step 5: Prepare the Claim for Third-Party Verification or Assurance

Identify whether your ESG report undergoes limited or reasonable assurance by an external auditor. If so, prepare a documentation package specifically for the launch emission claim.

Assurance levels:

- Limited assurance: Auditor performs fewer procedures, provides negative conclusion ("nothing has come to our attention...")

- Reasonable assurance: Extensive procedures including testing internal controls and source documents, provides positive conclusion

As regulatory regimes like the EU CSRD phase in requirements to move from limited to reasonable assurance, auditors will increasingly scrutinize Scope 3 supplier data. Be prepared to respond to auditor queries about:

- Completeness of Scope 3 reporting

- Whether upstream emissions from launch vehicle manufacture or hydrogen production have been excluded and why

- Data quality indicators (technological, temporal, geographical representativeness)

- Reliability of sources and verification procedures

When Should You Claim Zero-Emission Launch Status in an ESG Report?

Not every launch-related activity justifies a zero-emission designation. The claim is appropriate only when the combustion process itself produces no GHG Protocol-listed greenhouse gases and all supporting evidence is in hand.

Valid zero-emission claim scenarios:

- Companies in aerospace, satellite manufacturing, or scientific research that commission launches as part of core operations

- Launches using verified hydrogen-oxygen propulsion with documented zero CO2e emissions

- Supplier-specific emission data available — not just industry averages

- Reporting conducted under recognized GHG frameworks (GRI, IFRS S2, GHG Protocol, or TCFD)

Red flags that invalidate the claim:

- The launch provider uses mixed propellants or supplemental fuels at any stage

- Only part of the launch sequence is zero-emission (e.g., orbital circularization uses a solid rocket motor)

- Upstream emissions from hydrogen production are omitted without explicit boundary disclosure

- Documentation draws solely from marketing materials rather than technical specifications

- No third-party verification or engineering data supports the emissions figure

Real-world reporting practice helps clarify where the line sits. Airbus includes emissions from satellites delivered to customers under Scope 3 Category 11, accounting for both propellant production and combustion. Planet Labs similarly includes satellite launch emissions in its Scope 3 inventory under fuel and energy-related activities. Both cases demonstrate that boundary transparency — not just propellant type — determines whether a claim holds up to scrutiny.

What You Need Before Making a Zero-Emission Launch Claim

Preparation directly determines whether your claim will hold up under ESG disclosure standards or auditor review.

Propellant and Technical Documentation

Obtain written confirmation of propellant type and combustion byproduct data from the launch provider before the launch takes place. A zero-emission claim without this documentation is unverifiable and risks being flagged as greenwashing under regulations like the FTC Green Guides or the EU Green Claims Directive.

Providers using hydrogen and oxygen gas propellant — like Green Launch — should supply propellant specifications, combustion chemistry data, and emission factor calculations. Green Launch has demonstrated propellant capture efficiency exceeding 91%, reducing atmospheric release well beyond the water vapor byproduct alone.

ESG Framework and Reporting Structure

Confirm which reporting framework(s) govern your sustainability report — GRI, IFRS S2, TCFD, or the GHG Protocol. Understand the specific disclosure requirements for:

- Emission source categorization

- Data quality standards

- Methodology transparency

- Boundary setting and completeness

Each framework has distinct language requirements and measurement approaches that affect how you frame the zero-emission claim.

Internal Approval and Stakeholder Alignment

Once you've established which framework applies, internal sign-off is the next non-negotiable step. Before publication, the following functions should review and approve the claim:

- Sustainability/ESG team — verifies technical accuracy and framework alignment

- Legal counsel — assesses greenwashing exposure under applicable regulations

- Finance or compliance — confirms disclosure consistency with other public filings

Skipping this step is where organizations get into trouble: a claim that clears scientific review can still fail regulatory scrutiny if it's framed in ways that overstate scope or certainty.

The European Securities and Markets Authority (ESMA) defines greenwashing as practices where sustainability-related statements do not clearly and fairly reflect the underlying sustainability profile of an entity. Forward-looking pledges carry the highest exposure — auditors scrutinize them most closely when post-publication data doesn't match initial claims.

Key Parameters That Affect the Validity of Your Zero-Emission Launch Claim

The credibility of a zero-emission claim depends on several interconnected variables that ESG reviewers and auditors will scrutinize.

Propellant Composition and Purity

Even a primarily hydrogen-oxygen system may have trace impurities or use supplemental gases. The zero-emission claim must reflect the full combustion profile — not just the primary propellant.

Determine what compositional documentation your ESG framework requires to sustain a zero-emission designation. Request detailed specifications from your provider covering pressurization gases, ignition systems, and any auxiliary fuels.

GHG Scope and Boundary Setting

Where an emission sits in the GHG scope hierarchy determines how it is counted, compared, and audited. Scope 1 versus Scope 3 boundaries must be documented and applied consistently across reporting periods.

Inconsistent scope treatment between years triggers auditor queries and can require restatement — the GHG Protocol holds companies to consistent boundaries and methodologies year-over-year.

Emission Factor Source and Methodology

An unverified or self-reported emission factor of zero — without supporting methodology — will not meet the data quality standards of IFRS S2 or the GHG Protocol. Verify which source applies:

- Provider's own published data with technical basis

- Industry database or emission factor registry

- Third-party calculation or life cycle assessment

- ISO 14040/14044 compliant Environmental Product Declaration

Disclose which source was used and how it was verified.

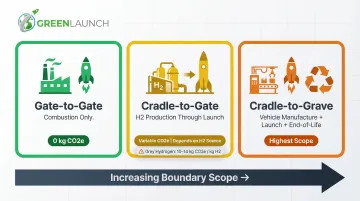

Upstream and Lifecycle Boundary Decisions

A launch may produce zero direct emissions, but generating the hydrogen propellant can be carbon-intensive depending on the production method. The IEA reports carbon intensity ranging from 0 kg CO2e/kg H2 for renewable electrolysis to 10–14 kg CO2e/kg H2 for unabated natural gas steam methane reforming.

Clearly document which lifecycle stages are included or excluded from the zero-emission claim:

- Cradle-to-gate (hydrogen production through launch)

- Gate-to-gate (combustion only)

- Cradle-to-grave (including launch vehicle manufacture and end-of-life)

The GHG Protocol Scope 3 Standard requires companies to account for all upstream (cradle-to-gate) emissions of purchased goods and services. If you claim a "zero-emission launch" but use grey hydrogen, you must still report the 10–14 kg CO2e/kg H2 generated during fuel production within your Scope 3 inventory.

Common Mistakes When Claiming Zero-Emission Launch in ESG Reports

Even well-intentioned ESG teams make avoidable errors when documenting zero-emission launch claims. Watch for these:

- Relying on marketing language alone instead of obtaining technical propellant data and the provider's emission calculation methodology

- Misclassifying launch emission scope — a third-party launch service is Scope 3, not Scope 1; auditors flag this inconsistency during assurance reviews

- Omitting methodology disclosure — failing to explain how the zero-emission designation was determined weakens credibility, even when the underlying data is accurate

- Treating a zero-emission direct launch as equivalent to "net-zero" or "carbon-neutral" — these are distinct claims; net-zero implies offset use and triggers additional compliance and verification requirements

- Ignoring upstream boundaries — claiming zero combustion emissions without disclosing carbon-intensive hydrogen production steps, or explaining why those steps fall outside the defined scope

Conclusion

Claiming a zero-emission launch in an ESG report is legitimate and defensible when built on verified propellant data, correct GHG scope classification, and framework-compliant disclosure language. The difference between a defensible claim and a retracted one is almost always preparation, not performance.

Most failed or challenged claims result from documentation gaps or unsupported terminology — not from the underlying emission profile of the launch itself. Companies that build audit-ready documentation practices now will be better positioned as space-related emissions attract greater scrutiny in corporate sustainability reporting.

That scrutiny is accelerating. California's SB 253 mandates Scope 3 reporting by 2027; the EU CSRD is rolling out phased requirements across large and listed companies. In that environment, the ability to substantiate claims with launch-provider-specific, technically verified data shifts from best practice to baseline requirement. Green Launch's hydrogen-oxygen propulsion model — with water vapor as its primary combustion byproduct — illustrates what that supplier-level documentation looks like in practice.

Frequently Asked Questions

What qualifies a space launch as zero-emission?

A space launch is zero-emission when its propellant combustion produces no GHG Protocol-listed greenhouse gases — such as hydrogen-oxygen propulsion, which releases only water vapor. This designation must be supported by technical documentation including propellant specifications and combustion chemistry data, not just marketing claims.

How do I determine whether a launch falls under Scope 1 or Scope 3 emissions?

Scope 1 applies only to launches conducted using equipment owned or directly controlled by your company. Launches contracted from a third-party provider are typically Scope 3 Category 1 (purchased goods and services) under the GHG Protocol, regardless of the emission profile.

What documentation do ESG auditors require to verify a zero-emission launch claim?

Auditors typically require:

- Propellant specification records

- Emission factor calculation or provider-supplied data

- Scope classification rationale

- Methodology note explaining how the zero-emission designation was derived

For reasonable assurance engagements, expect scrutiny of data quality, completeness, and traceability.

Can I claim zero emissions for a launch if I did not directly operate the vehicle?

Yes, the claim can be made for Scope 3 emissions, provided the launch provider supplies sufficient technical data to support the zero-emission designation and the claim is transparently framed as a supplier emission figure with appropriate methodology disclosure and boundary caveats.

Is ESG reporting mandatory in the USA?

The SEC adopted climate disclosure rules in March 2024 but voted to end its defence of these rules on March 27, 2025, meaning they are not currently in effect. However, California's SB 253 requires large US businesses operating in the state to report Scope 1 and 2 emissions by August 2026, with Scope 3 reporting following in 2027.

Is ESG still relevant in 2026?

Yes. As of 2026, 36 jurisdictions have adopted or are adopting ISSB standards (IFRS S1/S2), and the EU CSRD is in effect with major aerospace firms required to report comprehensively. Institutional investors representing over US$139 trillion in assets under management also remain committed to responsible investment principles.